House Affordability Calculator

Most buyers can comfortably afford a home where housing costs stay near 28–30% of income and total debts stay under about 36–43%. This house affordability calculator estimates a realistic home price using income, DTI rules, interest rate, taxes, insurance, and down payment.

People used this calculator

Your current platform: —

This total is global for all users (desktop and mobile) using this calculator on calculatorgeek.com.

How to Use These House Affordability Results

The estimated home price and monthly housing budget shown by this calculator are designed to help you explore comfortable affordability — not just the highest loan amount possible. Use the results as a starting point to compare scenarios, adjust down payment or interest rate assumptions, and understand how debt-to-income limits affect your budget.

If your back-end debt ratio is the limiting factor, reducing monthly debts or increasing your down payment may expand your affordability range. If interest rate changes have the largest impact, reviewing sensitivity scenarios can help you choose a safer home price range.

These results are most useful when combined with long-term planning, realistic monthly expenses, and professional advice before making a final home purchase decision.

House Affordability Calculator Overview

A house affordability calculator helps you estimate how much home you can realistically afford based on income, debts, interest rates, and expected housing costs. Instead of guessing a home price, it translates your financial details into a safer monthly mortgage range that aligns with common lending guidelines. In simple terms, most buyers can estimate affordability by keeping housing costs near one-third of gross income and total debts under common DTI guidelines, though actual limits vary by lender and country.

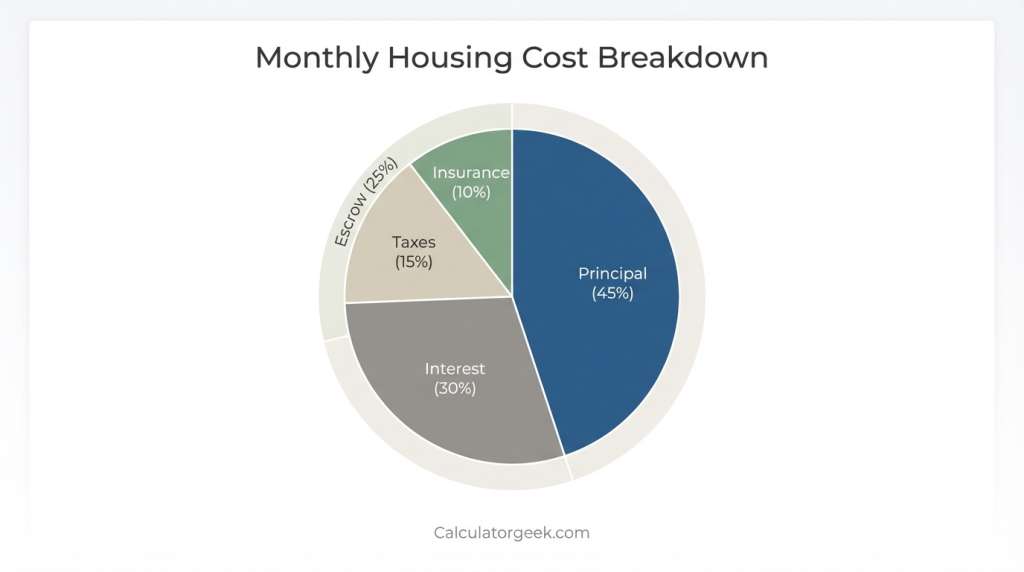

Buying a home is not just about the purchase price — it’s about managing total monthly housing costs, including principal, interest, taxes, insurance, and other expenses. Many buyers focus only on the mortgage amount and overlook debt-to-income limits, which can lead to unrealistic expectations or financial stress later.

This guide explains how the Calculatorgeek house affordability calculator works, what the numbers actually mean, and how to interpret the results using practical frameworks like the 28/36 rule. You’ll learn how income, down payment, loan term, and mortgage interest rates change affordability — plus see worked examples for different salary levels.

Whether you’re exploring a home affordability calculator, comparing a mortgage affordability calculator, or simply asking “how much house can I afford?”, this pillar guide is designed to give clear, decision-focused answers without hype or assumptions.

How Much House Can You Comfortably Afford?

Most buyers can estimate a comfortable home price by keeping total housing costs near 28–30% of gross monthly income and total debt payments under roughly 36–43%, depending on loan type and country guidelines. This house affordability calculator helps translate your income, debts, interest rate, and down payment into a realistic home price range rather than focusing only on the maximum loan amount.

Most people can comfortably afford a home when total housing costs stay below about one-third of income and overall debt payments remain within common debt-to-income guidelines.

What Is House Affordability?

House affordability means the price range of a home you can comfortably buy without putting pressure on your monthly budget. A house affordability calculator estimates this by comparing your income, debts, interest rate, and housing costs against widely used debt-to-income (DTI) guidelines.

In simple terms, affordability is not just about qualifying for a loan — it’s about maintaining financial stability after moving in. Lenders and financial planners usually look at how much of your gross monthly income goes toward housing payments and total debt obligations. According to housing finance guidance from organizations like the Consumer Financial Protection Bureau, many buyers aim to keep housing costs around 28–31% of income and total debt under roughly 36–43%, depending on loan type and country rules.

Why Affordability Matters More Than Home Price

A higher home purchase price does not always mean a better financial decision. The goal of a home affordability calculator is to help you balance three things:

- Monthly mortgage payments

- Existing debt payments

- Long-term financial flexibility

When buyers skip affordability planning, they often underestimate hidden costs such as property taxes, insurance, maintenance, or changes in mortgage interest rates. These factors affect total monthly housing costs, not just the mortgage principal.

Key Factors That Define Home Loan Affordability

Most mortgage affordability calculator models evaluate affordability using a combination of financial inputs:

- Income before taxes: Salary, bonuses, or consistent earnings

- Monthly debt payments: Credit cards, student loans, auto loans

- Down payment amount: Cash used upfront to reduce loan size

- Interest rate and loan term: Determines monthly repayment

- Property taxes and insurance: Included in escrow for realistic estimates

Because of these variables, two people earning the same income can afford very different home prices. A larger down payment, lower debt-to-income ratio, or longer repayment term can significantly change results inside a mortgage affordability calculator.

Affordability vs. Loan Approval

A house affordability calculator gives an estimate — not a loan approval. Lenders also consider factors like credit history, underwriting standards, and local market conditions before approving a mortgage loan.

Think of affordability as a planning tool that answers the question: “How much house can I afford while keeping my finances stable?” Instead of focusing on the maximum number a lender may offer, the goal is to find a sustainable monthly payment that fits your lifestyle.

How This House Affordability Calculator Works on CalculatorGeek

A house affordability calculator on Calculatorgeek estimates your realistic home budget by combining income, debts, interest rate, and housing expenses into a single affordability range. Instead of guessing a home price, it evaluates both front-end and back-end debt limits to show what you can comfortably afford.

Step-by-Step: How the Calculator Estimates Affordability

Most users begin by entering core financial details. The Calculatorgeek home affordability calculator then converts those inputs into an estimated home price range using common mortgage affordability formulas.

- Enter income before taxes — This represents your gross monthly income.

- Add monthly debt payments — Credit cards, student loans, and other obligations affect debt-to-income ratio.

- Choose interest rate and loan term — These determine the monthly mortgage repayment structure.

- Input down payment amount — A higher deposit reduces the mortgage principal and increases affordability.

- Include taxes and insurance — Property taxes, hazard insurance, or flood insurance help estimate total monthly housing costs.

Behind the scenes, the calculator compares housing costs to recommended debt-to-income ratios used across many mortgage loan guidelines.

Formula (Human-Readable Overview)

The mortgage affordability calculator applies a simplified affordability framework:

Affordable Monthly Housing Payment ≈

(Gross Monthly Income × Front-End Ratio) – Existing Debt Payments

Then it estimates a home purchase price by reversing the mortgage payment formula:

Estimated Home Price ≈ Loan Amount + Down Payment

Loan Amount derived from:

Monthly Payment, Interest Rate, and Mortgage Term

These calculations align with amortization principles similar to those used in the Amortization Calculator.

“Explain These Results” Micro-Copy

- Front-end cap vs back-end cap: The front-end ratio limits housing costs, while the back-end ratio considers all debts together.

- Why limiting factor matters: The stricter rule determines your final affordability number.

- What changing rate, term, or down payment does: Lower rates or larger deposits reduce monthly repayment, which increases the home price you may afford.

Two Example Interpretations

Example 1 — Income Mode:

$60,000 yearly income, minimal debts, 28/36 guideline → estimated home price around $180,000–$220,000 depending on taxes and rate assumptions.

Example 2 — Payment Mode:

If you know your comfortable monthly payment is $1,500, the calculator reverses the mortgage formula to estimate a home loan amount and total purchase price.

When to Use This Calculator

- Early home buying research

- Comparing repayment terms

- Planning a low down payment home loan

- Estimating monthly mortgage payments before speaking to lenders

When Not to Use It Alone

- Final loan approval decisions

- Situations with irregular income or major upcoming financial changes

- Markets with unusually high property taxes or insurance costs

Methodology Snapshot

- Uses common DTI benchmarks (28/36, 31/43 ranges)

- Includes taxes, insurance, and escrow-style estimates

- Treats results as planning guidance, not underwriting approval

Understanding the 28/36 Rule (And Other DTI Guidelines)

Most lenders estimate affordability using debt-to-income (DTI) guidelines, where housing costs stay near 28% of gross income and total debt payments stay near 36–43%. A house affordability calculator applies these limits to help you estimate a realistic mortgage payment without overextending your budget.

What the 28/36 Rule Means

The 28/36 rule separates affordability into two parts:

- Front-end debt ratio: Percentage of income used only for housing costs

- Back-end debt ratio: Percentage of income used for all debts combined

These guidelines are not strict laws, but they are commonly referenced benchmarks across many mortgage loan programs and underwriting models.

| DTI Component | What It Measures | Typical Range | Why It Matters |

|---|---|---|---|

| Front-End Ratio | Monthly housing costs vs gross monthly income | 28%–31% | Prevents mortgage payments from overwhelming income |

| Back-End Ratio | Total debts + housing costs vs income | 36%–43% | Shows overall financial risk to lenders |

A mortgage affordability calculator uses whichever ratio is stricter as the limiting factor. For example, if your debts are high, the back-end ratio may reduce the home price you can afford even if your income is strong.

Why DTI Ratios Affect Home Loan Affordability

Your debt-to-income ratio helps determine how lenders evaluate risk. Higher DTI levels may reduce the loan amount offered or require a higher down payment. A lower ratio often improves flexibility because it leaves room for unexpected expenses.

Key inputs that influence DTI calculations include:

- Gross monthly income (income before taxes)

- Monthly mortgage payments

- Student loans, credit cards, or auto loans

- Mortgage insurance or property taxes

Because these factors change over time, the home affordability calculator lets you adjust numbers quickly to see how affordability shifts.

Alternative DTI Models You May See

Different loan programs or countries may use slightly different thresholds:

- 31/43 guideline: Often used for certain insured loan programs

- 39/44 ranges: Sometimes used by lenders for higher-income borrowers

- Stress-test models: Used in some regions to evaluate affordability at higher interest rates

These variations explain why two lenders might give different results for the same borrower — and why a house affordability calculator free tool is best used as an estimate rather than a guarantee.

Quick Example of DTI in Action

If your gross monthly income is $6,000:

- Front-end limit (28%) → about $1,680 toward housing costs

- Back-end limit (36%) → about $2,160 toward total debts

If existing debts equal $700 monthly, your maximum housing payment may be closer to $1,460 because the back-end ratio becomes the limiting factor.

Two Ways to Estimate: Income Mode vs Payment Mode

A house affordability calculator usually works in two directions: starting from your income or starting from a comfortable monthly payment. Both approaches help answer the same question — how much house can I afford — but they suit different planning styles.

Income Mode — Estimate Based on Salary

Income mode calculates affordability using your earnings, debts, and typical debt-to-income ratio limits. This method is helpful when you are just beginning research and want a broad affordability range.

Most home affordability calculator tools ask for:

- Gross monthly income (income before taxes)

- Monthly debt payments

- Down payment amount

- Mortgage interest rate and loan term

- Property taxes and insurance estimates

The calculator then applies front-end and back-end DTI rules to estimate a monthly mortgage payment and approximate home purchase price.

When to use income mode:

- You know your salary but not your ideal payment yet

- You want a fast estimate of home loan affordability

- You are comparing different mortgage term scenarios

Payment Mode — Start With a Comfortable Monthly Budget

Payment mode reverses the process. Instead of starting with income, you enter the monthly housing payment you feel comfortable with. The mortgage affordability calculator then estimates the mortgage amount and home price based on interest rate and repayment term.

This approach is useful if:

- You already track monthly expenses

- You want to stay within a strict financial comfort zone

- You are comparing multiple property prices

Comparing Income Mode vs Payment Mode

| Mode | Best For | Key Advantage | Potential Limitation |

|---|---|---|---|

| Income Mode | First-time planning | Shows realistic affordability range | May feel abstract without a budget target |

| Payment Mode | Budget-focused buyers | Matches real monthly spending habits | Requires you to estimate a comfortable payment |

Many buyers use both modes together. They first calculate an estimate using income, then switch to payment mode to fine-tune monthly mortgage repayments.

How CalculatorGeek Handles Both Modes

The Calculatorgeek best home affordability calculator combines income-based and payment-based logic. It evaluates your inputs against DTI guidelines while also converting a chosen monthly repayment into a projected home purchase price.

This dual approach helps you understand affordability from two perspectives:

- What lenders may consider reasonable

- What your lifestyle can realistically support

How Down Payment Changes the House Price You Can Afford

A house affordability calculator shows that your down payment directly affects how much home you can afford because it reduces the mortgage principal and lowers monthly payments. Even a small increase in deposit amount can shift affordability more than many buyers expect.

Why Down Payment Size Matters

The down payment is the upfront cash used to purchase a home. A larger deposit lowers the home loan amount, which reduces interest costs and total monthly housing expenses.

Here’s how it influences affordability:

- Lower mortgage principal: Smaller loan balance means smaller monthly mortgage repayments

- Reduced mortgage insurance: Some loan programs require insurance when the down payment is low

- Improved debt-to-income ratio: Lower payments may help you stay within DTI limits

Many home affordability calculator tools let you experiment with different deposit levels to see how they affect the estimated home purchase price.

Example: How Deposit Amount Changes Affordability

| Home Price | Down Payment | Mortgage Amount | Estimated Monthly Payment* |

|---|---|---|---|

| $300,000 | 5% ($15,000) | $285,000 | $1,850 |

| $300,000 | 10% ($30,000) | $270,000 | $1,750 |

| $300,000 | 20% ($60,000) | $240,000 | $1,550 |

*Estimates assume a fixed interest rate and standard mortgage term. Actual payments vary based on property taxes, insurance, and mortgage interest rates.

Low Deposit vs Larger Down Payment

Some buyers explore low down payment home loan options to enter the market sooner. While this can increase short-term accessibility, it often leads to higher monthly payments and additional mortgage insurance costs.

A higher deposit may:

- Improve affordability range inside a mortgage affordability calculator

- Reduce the annual percentage rate impact over time

- Provide more flexibility if interest rates rise

How CalculatorGeek Uses Down Payment Inputs

Inside the Calculatorgeek house affordability calculator free tool, the deposit amount adjusts three key outputs:

- Total mortgage principal

- Monthly repayment estimate

- Maximum home price range based on DTI rules

Because affordability depends on both income and loan size, adjusting the down payment slider is often the fastest way to see realistic changes in affordability.

Practical Tip: Don’t Forget Closing Costs

Many first-time buyers focus only on the deposit amount. However, closing costs, taxes, and moving expenses may reduce the cash available for a down payment. Planning for these costs early helps avoid overstating affordability.

How Interest Rates, Taxes, and Insurance Affect “Real” Affordability

Your true home budget is not based only on the purchase price — it depends on interest rates, property taxes, and insurance costs that shape the total monthly payment. A house affordability calculator includes these factors to show realistic affordability instead of just a basic mortgage estimate.

Interest Rates Change Affordability Faster Than Home Price

Mortgage interest rates directly affect monthly mortgage payments. Even a small increase in rate can significantly raise repayment amounts because interest compounds over long loan terms.

For example:

- A 6% interest rate vs 7% rate on the same mortgage amount may increase payments by hundreds per month.

- Higher rates reduce the home purchase price you may afford under DTI limits.

That’s why many buyers revisit a mortgage affordability calculator when mortgage interest rates change — affordability shifts even if income stays the same.

Property Taxes and Insurance Are Part of Total Housing Costs

Many buyers underestimate non-mortgage expenses included in escrow accounts:

- Monthly property tax: Varies by location and property value

- Hazard insurance: Protects the home structure

- Flood insurance (where required): Can significantly affect monthly costs

- Mortgage insurance: Often required for low deposit mortgage options

A reliable home affordability calculator adds these costs into total monthly housing expenses so you see a realistic estimate rather than just principal and interest.

Why “Monthly Mortgage Payment” Isn’t the Full Picture

When people ask how much house can I afford, they often think only about loan repayment. In reality, affordability is based on:

- Mortgage principal and interest

- Taxes and insurance

- Escrow-related costs

- Existing monthly debt payments

Ignoring these factors can make a home seem affordable on paper but difficult to maintain long term.

Adjustable Inputs Help You Stress-Test Affordability

The Calculatorgeek best home affordability calculator lets you change assumptions like interest rate, repayment term, and deposit size. This helps you explore scenarios such as:

- What happens if rates rise by 1–2%

- How a longer loan term lowers monthly repayments but increases total interest

- How increasing deposit amount reduces insurance requirements

Testing different scenarios helps you understand “real affordability,” not just the highest home price you could qualify for.

Examples: How Much House Can You Afford at Different Incomes?

Most buyers use a house affordability calculator to translate income into a realistic home price range. While exact numbers vary based on debt, interest rate, and taxes, worked examples help show how affordability changes across different salary levels.

Quick Rule-of-Thumb Before the Examples

Many affordability models estimate housing costs around 28–30% of gross monthly income, with total debts often kept below about 36–43% depending on loan guidelines. These are planning benchmarks — not guarantees — but they help illustrate how a mortgage affordability calculator arrives at its results.

Example Assumptions Used Below

To keep comparisons consistent, these examples assume:

- Fixed interest rate scenario

- Standard mortgage term (e.g., 30 years)

- Moderate property taxes and insurance

- Minimal existing debt payments

Actual results inside a home affordability calculator may vary depending on your local taxes, insurance rates, or credit profile.

Estimated Affordability by Income Level

| Annual Income | Estimated Monthly Housing Budget | Approximate Home Price Range | Example Down Payment |

|---|---|---|---|

| $60,000 | $1,400 – $1,600 | $180,000 – $230,000 | 10% |

| $80,000 | $1,900 – $2,200 | $250,000 – $320,000 | 10% |

| $100,000 | $2,400 – $2,800 | $330,000 – $420,000 | 10% |

These ranges illustrate how higher income increases affordability — but only when debt-to-income ratios remain balanced.

Worked Example 1 — $60K Income Using 28/36 Guideline

- Gross monthly income ≈ $5,000

- Front-end housing limit (28%) ≈ $1,400

- Estimated home price range ≈ $200K depending on interest rate

If interest rates rise, the same income may support a lower home purchase price even though salary remains unchanged.

Worked Example 2 — Same Income With Higher Down Payment

Using the same $60K income but increasing the down payment from 5% to 20%:

- Mortgage principal decreases

- Monthly mortgage repayments drop

- Affordability range increases because DTI limits improve

This is why adjusting deposit amount inside a house affordability calculator free tool can change results quickly.

Worked Example 3 — Payment-Based Mode

If a buyer earning $80K decides their comfort level is a $2,000 monthly repayment, the calculator reverses the mortgage formula:

- Determines mortgage amount supported by that payment

- Adds deposit amount

- Estimates total home purchase price

This method answers the practical question: How much house can I afford while keeping monthly costs stable?

These comparisons help show that interest rate changes often affect affordability more than small changes in income or home price.

Country-Specific Notes (US, Canada, UK, Australia)

House affordability rules vary by country because lending standards, stress tests, and housing costs differ. A house affordability calculator gives a general estimate, but understanding regional guidelines helps you interpret results more accurately.

United States — DTI Ratios and Loan Program Flexibility

In the US, many lenders use debt-to-income ratios around 28/36 or slightly higher depending on loan type. Buyers may also see options like low down payment home loans, which can increase accessibility but may include mortgage insurance.

Common factors affecting home loan affordability in the US:

- Annual percentage rate differences between fixed and adjustable loans

- Property tax variations by state

- Insurance requirements for certain regions

Because of these variables, using a mortgage affordability calculator with realistic tax and insurance estimates can produce more accurate planning results.

Canada — Stress Tests and Interest Rate Buffers

Canadian lending often includes a mortgage stress test. This means affordability is evaluated at a higher interest rate than the actual mortgage rate to ensure borrowers can handle future increases.

Key considerations:

- Mortgage-to-income ratio guidelines

- Stress-tested monthly mortgage payments

- Regional housing price differences

When using a home affordability calculator, adding a slightly higher interest rate can simulate this stress-test approach.

United Kingdom — Income Multiples and Affordability Checks

UK lenders frequently use income multiples combined with affordability checks that consider monthly expenses and financial commitments.

Typical influences on affordability:

- Income before taxes and employment stability

- Mortgage repayment term length

- Household spending patterns

A house affordability calculator free tool helps estimate repayment ranges, but lenders may also review living expenses during underwriting.

Australia — Living Expense Assessments

Australian lenders often analyze detailed spending patterns rather than relying solely on debt ratios. This means affordability may depend on both income and verified lifestyle costs.

Important factors include:

- Verified monthly expenses

- Interest rate buffers

- Deposit size and loan-to-value ratio

Because living costs vary significantly, adjusting repayment assumptions inside a best home affordability calculator can provide a more realistic affordability estimate.

Why Country Differences Matter

Even though affordability guidelines differ, most systems still rely on the same core idea: balancing income, debt-to-income ratio, and total monthly housing costs. The Calculatorgeek house affordability calculator provides a flexible framework that works across regions by letting you adjust interest rates, taxes, and repayment assumptions manually.

Common Mistakes People Make With Affordability Calculators

Most people use a house affordability calculator to get quick answers, but small misunderstandings can lead to unrealistic expectations. Knowing the common mistakes helps you interpret results more accurately and avoid overestimating what you can comfortably afford.

Mistake 1 — Focusing Only on Mortgage Amount

Many buyers look only at the mortgage principal and forget about taxes, insurance, and escrow costs. A reliable home affordability calculator includes total monthly housing costs, not just loan repayment.

What to check:

- Monthly property tax estimates

- Hazard or flood insurance

- Mortgage insurance if using a low deposit mortgage

Ignoring these costs may make a home appear affordable even when the real monthly payment is much higher.

Mistake 2 — Using Net Income Instead of Gross Income

Most affordability models calculate debt-to-income ratio using income before taxes. Entering take-home pay instead of gross income can underestimate affordability and distort comparisons between different loan scenarios.

Mistake 3 — Not Updating Interest Rate Assumptions

Mortgage interest rates change frequently. If you use outdated rate assumptions, the mortgage affordability calculator may show a home price range that no longer reflects current conditions.

Even a small rate change can:

- Increase monthly mortgage repayments

- Reduce the maximum mortgage amount supported by DTI rules

Mistake 4 — Ignoring Existing Monthly Debt Payments

Credit cards, student loans, and auto loans directly affect the back-end debt ratio. Some buyers forget to include these, which can make the calculator results look more optimistic than reality.

To improve accuracy, include:

- Minimum credit card payments

- Personal loans

- Student loan obligations

Mistake 5 — Assuming the Calculator Equals Loan Approval

A house affordability calculator free tool estimates affordability — it does not guarantee approval from mortgage lenders. Approval decisions also consider credit history, underwriting policies, and local market factors.

Edge Cases That Can Change Results

Certain situations may require extra caution when interpreting results:

- Irregular income or commission-based work

- Second home affordability scenarios

- High-cost insurance regions

- Adjustable rate mortgage structures

If you fall into one of these categories, adjusting assumptions or testing multiple scenarios inside the best home affordability calculator can help you understand the full range of affordability.

When to Use This Calculator — And When Not To

A house affordability calculator is most useful during early planning and comparison stages. It helps you understand a realistic home price range, but it works best when used alongside broader financial research — not as a final approval tool.

When to Use a House Affordability Calculator

Use the calculator when you want a structured estimate of home loan affordability based on income, debts, and housing costs.

Common scenarios include:

- Exploring how much house can I afford before contacting mortgage lenders

- Comparing repayment terms and mortgage interest rates

- Planning a low down payment home loan strategy

- Stress-testing affordability by adjusting deposit amount or interest rate

Many buyers also pair the calculator with tools like a Debt-to-Income Ratio Calculator to calculate your exact DTI and see how small changes affect eligibility.

When Not to Rely on It Alone

A mortgage affordability calculator provides guidance — not underwriting decisions. Some situations require deeper financial review:

- Final mortgage approval or pre-approval decisions

- Complex financial profiles or fluctuating income

- Homes with unusually high property taxes or insurance costs

- Situations involving major upcoming financial changes

If you’re preparing for a purchase, it may help to combine affordability estimates with other tools, such as a Mortgage Payment Calculator to preview detailed monthly repayments or a Closing Costs Calculator to estimate upfront expenses.

Adjustable Defaults and Assumptions

Calculatorgeek’s house affordability calculator free model uses adjustable assumptions so you can tailor estimates to your situation:

- Interest rate and repayment term

- Down payment percentage

- Property tax and insurance estimates

- Debt-to-income guideline ranges

Because these assumptions influence results, testing multiple scenarios helps you understand how affordability changes rather than relying on a single number.

Key Takeaway

Think of the calculator as a planning framework — not a guarantee. It helps you explore possibilities safely, identify realistic monthly mortgage payments, and prepare better questions before speaking with lenders or advisors.

Methodology & Sources

This house affordability calculator guide is built around commonly referenced affordability frameworks used in housing finance education and lending models. The goal is to provide a realistic planning estimate — not a loan approval — by combining income data, debt-to-income guidelines, and total monthly housing costs.

How Affordability Is Estimated

The Calculatorgeek home affordability calculator uses a structured methodology based on these principles:

- Housing costs are compared against front-end and back-end debt ratios.

- Total monthly housing costs include principal, interest, taxes, and insurance (often called escrow costs).

- Loan size is estimated using amortization-style calculations similar to standard mortgage repayment models.

- Inputs like down payment amount, mortgage term, and interest rate adjust the projected home purchase price.

These calculations reflect widely referenced benchmarks used by housing authorities and mortgage education resources, where affordability is evaluated as a percentage of gross monthly income rather than take-home pay.

Core Assumptions Used in Examples

To keep worked examples consistent throughout this pillar guide, the following assumptions were applied:

- Moderate property tax and hazard insurance estimates

- Stable fixed-rate mortgage scenario

- Typical debt-to-income guideline ranges (28/36 and similar models)

- Minimal existing debt unless stated otherwise

Because local taxes, insurance costs, and mortgage interest rates vary widely, results from any mortgage affordability calculator should be treated as planning guidance rather than precise financial advice.

What Affordability Means in This Guide

- Affordability represents a comfort-focused estimate, not the highest loan amount possible.

- Debt-to-income ratio benchmarks help illustrate common lender evaluation methods.

- Examples are designed to be educational and easily adjustable within the Calculatorgeek tool.

Why This House Affordability Calculator Is More Realistic

Many online tools estimate only the loan amount, but this house affordability calculator focuses on real monthly affordability by including additional housing costs and practical safeguards.

- Includes real housing costs: property taxes, insurance, HOA fees, and optional maintenance buffer so results reflect total monthly housing expenses — not just principal and interest.

- Shows both DTI limits: front-end (housing only) and back-end (housing plus all debts), helping you understand what actually limits your affordability.

- Stress-tests your budget: optional interest-rate buffer shows how affordability changes if rates increase.

- Provides sensitivity analysis: compare scenarios like rate changes, loan term adjustments, or down-payment variations instead of relying on a single fixed number.

This approach helps you focus on comfortable long-term affordability rather than the maximum loan amount a lender might approve. Unlike basic mortgage calculators that estimate only loan size, this tool focuses on realistic monthly affordability by including total housing costs and stress-testing scenarios.

How Lenders Decide How Much House You Can Afford

Most mortgage lenders do not look only at your income when deciding how much home you can afford. Instead, they evaluate a combination of debt-to-income ratios, housing costs, and financial stability to estimate whether monthly payments remain manageable over time.

Debt-to-Income Ratio (DTI)

Lenders typically compare your monthly debts to your gross monthly income using two key measurements:

- Front-end ratio: housing costs compared to income.

- Back-end ratio: housing costs plus all other debts compared to income.

Many affordability models reference guideline ranges such as 28–31% for housing costs and roughly 36–43% for total debt obligations, though actual limits vary by country and loan program. Debt-to-income ratio is simply the percentage of your gross monthly income that goes toward debt payments, including housing costs.

Income and Monthly Debt Payments

Your income before taxes, along with recurring debts like student loans, credit cards, or car payments, directly affects how much mortgage payment fits within acceptable risk levels. Even with a strong salary, higher existing debts may reduce the maximum home purchase price.

Interest Rate and Loan Term

Mortgage interest rates and repayment term length change how much principal you can borrow for the same monthly payment. Lower rates or longer loan terms generally increase affordability, while higher rates reduce the home price you may qualify for.

Down Payment and Reserves

A larger down payment reduces the loan amount and monthly repayment, which may improve affordability and lower mortgage insurance costs. Some lenders also consider financial reserves or savings when evaluating overall risk.

This house affordability calculator reflects many of these factors by comparing front-end and back-end limits, incorporating housing expenses beyond the mortgage itself, and allowing you to test how changes in rate, term, or down payment affect your affordability range.

What Happens If You Stretch Your Budget Too Far?

Buying a home at the highest price a lender approves does not always mean the payment will feel comfortable long term. Stretching your housing budget too far can increase financial pressure, especially if interest rates change or unexpected expenses arise.

Higher Monthly Stress

When total housing costs approach the upper limit of your debt-to-income ratio, small changes — such as rising insurance costs, property taxes, or maintenance — can quickly reduce financial flexibility. This may leave less room for savings, emergencies, or lifestyle expenses.

Less Flexibility If Rates Change

Some buyers qualify based on current interest rates, but higher future rates or refinancing conditions may increase monthly payments. Testing different scenarios inside a house affordability calculator helps reveal how sensitive affordability is to rate changes.

Increased Risk During Life Changes

Major life events like job transitions, moving expenses, or new financial commitments can feel more challenging when housing costs are already near the maximum limit. Maintaining a comfortable affordability range instead of the highest possible home price can reduce long-term stress.

How to Stay Within a Comfortable Range

- Aim for housing costs that leave room for savings and unexpected expenses.

- Compare multiple scenarios using sensitivity results instead of focusing on a single number.

- Consider a slightly lower home price if your back-end debt ratio is already high.

- Use tools like the Debt-to-Income Ratio Calculator or Mortgage Payment Calculator to understand how small changes affect monthly payments.

This house affordability calculator is designed to help you explore realistic scenarios so you can choose a home price that supports long-term financial stability, not just loan approval.

What This House Affordability Calculator Does Not Predict

A house affordability calculator helps estimate a comfortable home price range based on income, debts, and housing costs, but it cannot account for every real-world financial factor. Understanding what the calculator does not predict can help you use the results more effectively.

Future Market Changes

Property taxes, insurance premiums, and maintenance costs may change over time depending on local market conditions or policy updates. While this calculator includes adjustable estimates, actual costs may vary after purchase.

Personal Spending Habits

Affordability models use general debt-to-income guidelines, but individual spending patterns — such as travel, childcare, or lifestyle expenses — can affect how comfortable a monthly payment feels.

Loan Approval Decisions

Mortgage lenders evaluate additional factors such as credit history, employment stability, underwriting policies, and financial reserves. Because of this, the maximum home price shown by a calculator is an estimate rather than a guaranteed loan approval.

Unexpected Life Events

Changes in income, relocation plans, or major financial commitments can influence long-term affordability. Testing different scenarios inside the calculator can help you prepare for potential changes, but no tool can predict future personal circumstances.

Using this house affordability calculator alongside professional advice and careful budgeting can help you interpret results responsibly and make informed housing decisions.

The goal of this house affordability calculator is to help you explore realistic price ranges so you can plan with confidence rather than relying on maximum loan estimates alone.

Limitations & Disclaimer

A house affordability calculator provides planning estimates based on the financial details you enter, but it cannot account for every personal or market variable. Results should be viewed as educational guidance rather than financial, legal, or lending advice.

Affordability depends on many factors beyond basic calculations, including underwriting policies, credit history, regional housing costs, and changing mortgage interest rates. Because of this, the estimated home purchase price or monthly mortgage payment shown in a home affordability calculator may differ from what mortgage lenders ultimately approve.

Key limitations to keep in mind:

- Estimates rely on adjustable assumptions such as interest rate, repayment term, and property tax inputs.

- Local insurance costs, escrow rules, and loan program requirements may vary by region.

- Debt-to-income guidelines used in the calculator represent common benchmarks, not universal rules.

- Financial situations involving irregular income, major life changes, or complex debt structures may require personalized review.

“Tools information on Calculatorgeek is provided for general guidance and educational purposes only.”

Using a mortgage affordability calculator alongside professional advice can help you interpret results responsibly and understand the difference between estimated affordability and actual loan qualification.

Ad & Content Safety Note

This house affordability calculator article is written for educational and informational purposes with a focus on responsible financial planning. It avoids income promises, investment guarantees, or exaggerated claims about qualifying for a mortgage loan.

Calculatorgeek content is designed to be AdSense-safe by presenting neutral explanations, realistic examples, and balanced affordability guidance. Readers should always compare multiple scenarios and verify details with qualified financial professionals before making housing decisions.

Author & Reviewer

Author

Name: Daniel Carter

Role: Editor

Credential: Personal Finance Content Editor

Reviewer

Name: Olivia Bennett

Role: Financial Content Reviewer

Credential: Certified Mortgage & Housing Finance Analyst

FAQs

How much house can I afford with my salary using a house affordability calculator?

Most people can comfortably afford a home where total housing costs stay around 28–30% of gross income and total debts remain under roughly 36–43%. A house affordability calculator estimates this range by combining income, debt-to-income ratio, and mortgage interest rate assumptions into a realistic monthly payment.

What is the 28/36 rule in a house affordability calculator?

The 28/36 rule separates affordability into two limits. The front-end ratio suggests housing costs stay near 28% of income, while the back-end ratio suggests all debts stay near 36%. A mortgage affordability calculator uses these guidelines to estimate a balanced home loan amount rather than just the maximum loan size.

How does DTI affect house affordability?

Debt-to-income ratio directly influences how much home you may afford. Higher monthly debt payments reduce the housing budget allowed within DTI guidelines, which lowers the estimated home purchase price shown by a home affordability calculator.

How much should I put down on a house?

A larger down payment usually lowers monthly mortgage repayments and may reduce mortgage insurance costs. Many buyers aim for 10–20%, but the ideal deposit amount depends on income stability, loan program rules, and total monthly housing costs calculated inside a house affordability calculator free tool.

Does my credit score affect how much house I can afford?

Yes, credit profile can influence interest rate, loan eligibility, and required deposit size. While a house affordability calculator estimates affordability using income and debts, actual loan offers from mortgage lenders may vary based on credit history and underwriting review.

What expenses are included in monthly housing costs?

Typical affordability models include principal, interest, property taxes, hazard insurance, and sometimes mortgage insurance. These combined costs determine total monthly housing expenses used by a mortgage affordability calculator to estimate realistic affordability.

How much house can I afford based on my income?

A common starting point is keeping monthly mortgage payments within about one-third of gross income, but the exact amount depends on debts, down payment, and mortgage term. Using a house affordability calculator helps translate income into a practical home price range rather than relying on rough rules alone.

References

- Consumer Financial Protection Bureau (CFPB) — Home Buying & Mortgage Affordability Guidance

- Federal Housing Administration (FHA) — Debt-to-Income Ratio and Mortgage Qualification Guidelines

- Financial Consumer Agency of Canada (FCAC) — Mortgage Affordability and Budgeting Resources

- Australian Securities and Investments Commission (ASIC) — Mortgage and Home Loan Cost Education

Unlike basic mortgage calculators, this tool evaluates both loan qualification and real-world monthly affordability.