Capital Gains Tax Calculator

Estimate capital gains tax on immovable property in Pakistan using acquisition date, disposal date, property type, and filer (ATL) status — with instant auto-updating results.

Results

Formula

People used this calculator

Your current platform: —

Global counter (server-side).

Intro

A capital gains tax calculator helps you estimate the tax you may owe when you sell immovable property in Pakistan, using the rules that depend on acquisition date, property type, and filer (ATL) status. If you skip any of these inputs, you can easily apply the wrong rate—especially where the law switches treatment for properties acquired on or after 1 July 2024.

This guide explains what capital gains tax is, how a calculator should work, what inputs matter most, and how to interpret results like effective rate, tax amount, and net proceeds—without relying on guesswork.

Capital Gains Tax Calculator

A capital gains tax calculator estimates the capital gain, selects the correct tax regime based on your acquisition date, and applies the relevant capital gains tax rate to show your likely capital gains tax and net proceeds. for.

In practical terms, your result usually depends on just three decisions:

- When you bought the property

- Bought on or after 1 July 2024: for people on the Active Taxpayers List (ATL), the gain is taxed at a flat 15%, regardless of holding period.

- Bought on or before 30 June 2024: rates depend on property type and holding period, with slabs that can reduce to 0% after certain holding thresholds.

- What you sold

- Open plot vs constructed property vs flat can change the slab rate for the same holding period.

- Whether you are ATL (filer) at disposal

- For post–1 July 2024 acquisitions, ATL status is a key switch that affects which rate framework applies.

What the calculator should output (and what to copy/share):

- Capital gain (PKR) = sale value − cost basis

- Applicable regime = “Pre–1 Jul 2024 (holding slabs)” or “Post–1 Jul 2024 (ATL-based)”

- Holding period (when relevant)

- Tax rate (as %)

- Capital gains tax (PKR)

- Net proceeds after CGT (PKR)

What Is Capital Gains Tax on Property in Pakistan?

Capital gains tax is the tax applied to the profit (gain) you make when you sell immovable property for more than your purchase cost. In simple terms, if your sale value is higher than your cost basis, the difference is your capital gain, and a CGT rate may apply.

Here’s what matters most for property capital gains tax in Pakistan:

- CGT is gain-based, not sale-price-based.

The calculator focuses on the profit portion (sale minus cost), not the full sale amount. - The acquisition date can switch the entire rule set.

Property acquired before 1 July 2024 generally uses holding-period slabs by property type, while property acquired on/after 1 July 2024 follows an updated approach where filer status becomes more central. - Property type can change the slab rate.

Open plots, constructed property, and flats may follow different holding-period tables for older acquisitions. - ATL (filer) status affects how the rate is applied for newer acquisitions.

For many cases after 1 July 2024, ATL status can determine whether a flat rate applies or a higher schedule is relevant.

Practical takeaway: A capital gains tax calculator is most useful when it forces the correct sequence: identify regime → compute gain → apply rate schedule → show tax and net proceeds.

How to Use a Capital Gains Tax Calculator for Properties Sales

A capital gains tax calculator works best when you enter inputs in the same order the tax rules depend on them: acquisition date first, then property type, then values, then ATL status (if needed). That sequence prevents the most common rate-selection errors.

Step-by-step (decision-support checklist)

- Select property type

Pick the closest match: Open plot, Constructed property, or Flat.

This matters most for properties acquired before 1 July 2024, where the slab rate can vary by type. - Enter acquisition date and disposal date

These two dates decide whether holding-period slabs apply and whether “post–1 July 2024” treatment applies.

Also check: disposal date must not be earlier than acquisition date. - Enter sale value and cost basis (PKR)

- Sale value: the consideration you received.

- Cost basis: your purchase cost (and in a manual method, often plus allowable expenses—see the manual section later).

- Choose ATL (filer) status (if prompted)

For properties acquired on/after 1 July 2024, ATL status is a key switch for which schedule applies.

If your calculator requires it, select it explicitly rather than guessing. - Review the outputs (use “effective rate” as a sanity check)

A good calculator will show:

- capital gain

- regime (pre/post cutoff)

- holding period (when relevant)

- tax rate / effective rate

- tax payable

- net proceeds after CGT

If the “regime” looks wrong, fix dates first—don’t adjust numbers to force a result.

Voice-friendly summary

If you only remember one rule: dates drive the regime, and regime drives the rate—so always confirm acquisition date before you trust the tax rate.

Inputs That Change Your Result Most

The biggest changes in a capital gains tax calculator come from inputs that affect which rule set applies and which rate table is used—not from small tweaks to the numbers.

1) Acquisition date (most important)

Your acquisition date determines whether the calculator uses:

- Pre–1 July 2024: holding-period slabs by property type, or

- On/after 1 July 2024: filer-status and entity-type based treatment (no holding slabs).

If your acquisition date is wrong, everything else can be “correct” and the final CGT still ends up wrong.

2) Property type (open plot vs constructed vs flat)

For older acquisitions (pre–1 July 2024), property type can move you into a different slab rate for the same holding period.

This is one of the most common reasons two people with the same holding period get different CGT results.

3) Holding period (derived from acquisition + disposal date)

Holding period drives the slab for pre–1 July 2024 properties.

Even a few days can shift you between two bands (for example, crossing from “≤2 years” to “>2 years”).

4) ATL (Active Taxpayer List) status

For newer acquisitions (on/after 1 July 2024), ATL status often decides whether the estimate uses a flat filer rate or the higher non-filer schedule.

5) Legal entity type (individual/AOP vs company)

If the post–1 July 2024 path is triggered and the user is non-ATL, entity type can change the applied framework (individual/AOP progressive approach vs company rate assumptions).

6) Sale value and cost basis (the actual gain)

These don’t just scale the output. They can change:

- whether the gain is positive (taxable) or a loss (often shown as 0 CGT in basic estimators),

- whether a “surcharge-style” rule might become relevant (depending on how the calculator is designed).

Inputs That Change Your Result Most

The biggest changes in a capital gains tax calculator come from inputs that affect which rule set applies and which rate table is used—not from small tweaks to the numbers.

1) Acquisition date (most important)

Your acquisition date determines whether the calculator uses:

- Pre–1 July 2024: holding-period slabs by property type, or

- On/after 1 July 2024: filer-status and entity-type based treatment (no holding slabs).

If your acquisition date is wrong, everything else can be “correct” and the final CGT still ends up wrong.

2) Property type (open plot vs constructed vs flat)

For older acquisitions (pre–1 July 2024), property type can move you into a different slab rate for the same holding period.

This is one of the most common reasons two people with the same holding period get different CGT results.

3) Holding period (derived from acquisition + disposal date)

Holding period drives the slab for pre–1 July 2024 properties.

Even a few days can shift you between two bands (for example, crossing from “≤2 years” to “>2 years”).

4) ATL (Active Taxpayer List) status

For newer acquisitions (on/after 1 July 2024), ATL status often decides whether the estimate uses a flat filer rate or the higher non-filer schedule.

5) Legal entity type (individual/AOP vs company)

If the post–1 July 2024 path is triggered and the user is non-ATL, entity type can change the applied framework (individual/AOP progressive approach vs company rate assumptions).

6) Sale value and cost basis (the actual gain)

These don’t just scale the output. They can change:

- whether the gain is positive (taxable) or a loss (often shown as 0 CGT in basic estimators),

- whether a “surcharge-style” rule might become relevant (depending on how the calculator is designed).

Below is the standard holding-period slab table widely published for Pakistan property CGT.

| Holding period (years) | Open plots | Constructed property | Flats |

|---|---|---|---|

| ≤ 1 | 15% | 15% | 15% |

| > 1 to ≤ 2 | 12.5% | 10% | 7.5% |

| > 2 to ≤ 3 | 10% | 7.5% | 0% |

| > 3 to ≤ 4 | 7.5% | 5% | 0% |

| > 4 to ≤ 5 | 5% | 0% | 0% |

| > 5 to ≤ 6 | 2.5% | — | — |

| > 6 | 0% | — | — |

How to read this table (quick sanity checks):

- For flats, CGT reaches 0% after >2 years in this slab table.

- For constructed property, CGT reaches 0% after >4 years.

- For open plots, CGT steps down gradually and reaches 0% after >6 years.

Slabs for property bought on or after 1 July 2024

For properties acquired on or after 1 July 2024, the commonly stated headline rule is:

- ATL (filer): Flat 15% CGT on gain, regardless of holding period.

- Non-ATL: tax is applied using the relevant general schedules (e.g., Division I for individuals/AOPs and Division II for companies), and public summaries commonly note a minimum of 15% for individuals/AOPs in this context.

What this means for a pakistan capital gains tax calculator:

The calculator must ask for ATL status and, for non-ATL cases, typically needs an entity type to choose the right schedule path.

How to Calculate Capital Gains Tax on Real Estate

To calculate CGT manually, you first compute your capital gain, then apply the applicable tax rate based on your acquisition date, holding period (if relevant), property type, and ATL status.

Step 1: Calculate your capital gain

Capital Gain = Sale Price − (Purchase Price + Allowable Expenses)

In a basic calculator, “allowable expenses” may be simplified or excluded. In real-world filing, expenses can include certain documented costs tied to acquiring or transferring the asset (keep receipts and official documents).

Step 2: Apply the correct CGT rate

CGT Payable = Capital Gain × Applicable Tax Rate

The “applicable tax rate” is where most mistakes happen. A capital gains tax calculator reduces errors by selecting the correct rate path automatically.

Worked example (simple and practical)

- Purchased (cost): PKR 5,000,000

- Sold (sale value): PKR 8,000,000

- Holding period: about 2.5 years

- Capital gain: PKR 3,000,000

Case A: Bought before 1 July 2024 (holding-period slabs apply)

If it’s an open plot and the holding period falls in the >2 to ≤3 years band, the slab rate is 10%.

Tax = 3,000,000 × 10% = PKR 300,000

Case B: Bought on/after 1 July 2024 (ATL-driven approach)

If you are ATL (filer) and the calculator applies a flat 15% on capital gain:

Tax = 3,000,000 × 15% = PKR 450,000

Quick sanity checks before trusting the result

- If sale value ≤ cost, your gain is zero or negative. Many calculators show 0 CGT (but keep records in case other rules apply).

- If your rate looks unexpectedly high or low, re-check:

- acquisition date (most common error)

- property type (open plot vs constructed vs flat)

- ATL selection (for newer acquisitions)

Formula

A capital gains tax calculator is essentially a rule-based calculator that follows a small set of formulas, then chooses the correct tax rate from the right schedule.

Core formulas (human-readable)

1) Capital gain

Capital Gain = Sale Value − Cost Basis

In a more detailed manual calculation, “cost basis” can include certain allowable acquisition/transfer expenses you can document, but many online calculators use a simplified cost basis input.

2) Holding period (when applicable)

Holding Period = Disposal Date − Acquisition Date

This is typically converted into years (and sometimes months/days) to select the correct slab for pre–1 July 2024 acquisitions.

3) Capital gains tax

CGT Payable = Capital Gain × Applicable CGT Rate

4) Net proceeds after CGT

Net Proceeds = Sale Value − CGT Payable

(Some people also subtract fees, commissions, or other costs separately. This calculator keeps net proceeds focused on CGT.)

Rate selection logic (what a good calculator does)

A pakistan capital gains tax calculator should choose the rate in this order:

- Check acquisition cutoff date

- On/after 1 July 2024: use ATL-driven path (flat filer rate commonly summarized as 15%).

- On/before 30 June 2024: use holding-period slabs by property type.

- If pre–1 July 2024, select slab by:

- property type (open plot / constructed / flat)

- holding period band (≤1, >1–≤2, etc.)

- If post–1 July 2024, select treatment by:

- ATL status (filer vs non-filer)

- entity type (individual/AOP vs company) if required by the calculator’s estimation path

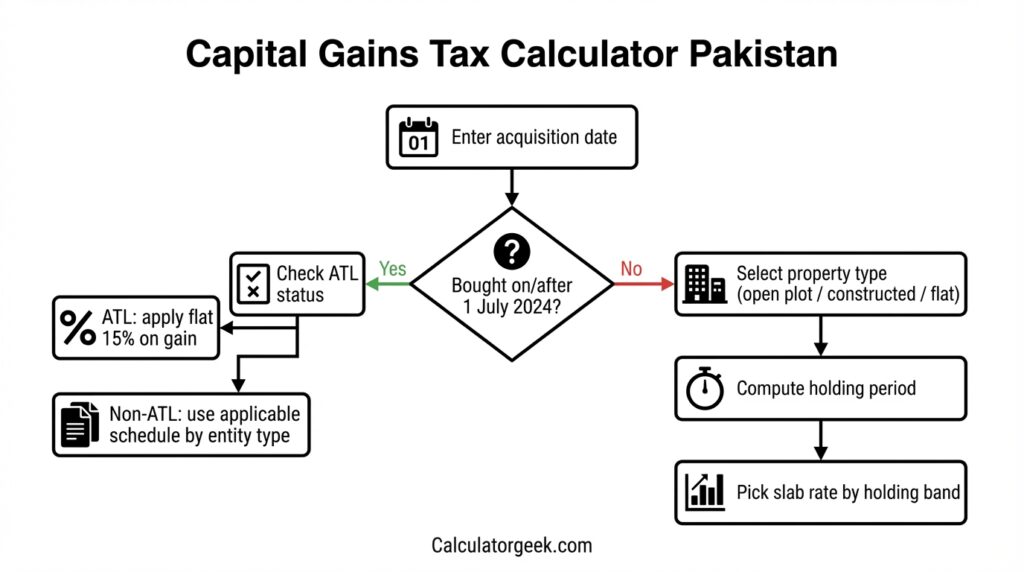

How the CalculatorGeek Capital Gains Tax Calculator Works

The CalculatorGeek tool is designed to behave like a capital gains tax calculator should: it chooses the correct rule path first, then calculates the gain, then applies the rate, and finally shows a clear breakdown you can copy or share.

1) It confirms the correct tax regime before calculating the rate

The calculator uses your acquisition date as the “switch”:

- Bought on or before 30 June 2024: it uses holding-period slabs by property type.

- Bought on or after 1 July 2024: it follows an ATL-driven path, where filer status becomes the key factor.

This prevents the most common error: applying a holding-period rate to a post-cutoff acquisition (or vice versa).

2) It calculates capital gain in one clear step

Once the regime is known, the calculator computes:

- Capital gain = sale value − cost basis

If your gain is negative (sale value below cost), the results area should show a neutral message and avoid presenting “tax payable” as a confident number.

3) It applies the rate in a way users can audit

A reliable capital gains tax calculator should show why a rate was selected by displaying:

- regime label (pre/post cutoff)

- holding period (when relevant)

- property type selection

- filer status selection (when relevant)

That “audit trail” is what makes the result decision-support rather than a black box.

4) Results update instantly (no “calculate” button)

CalculatorGeek updates results automatically on every input change, so you can:

- test different disposal dates to see slab changes

- compare open plot vs constructed property

- model the impact of a higher cost basis or lower sale value

This is especially helpful when you’re planning timing and want to see how the capital gains tax calculator output changes with holding period thresholds.

5) Copy, share, and reset are built for real workflows

The results panel includes:

- Copy buttons for each output line

- Copy all outputs for pasting into messages or notes

- Share result to generate a link (only when inputs are valid)

- Clear all to reset inputs and outputs cleanly

This makes it easier to keep a record of scenarios you compare.

Examples

These examples show how a capital gains tax calculator can produce different outcomes from the same sale and cost values—simply because the acquisition date and rate path differ.

Example 1: Open plot bought before 1 July 2024 (holding-period slabs)

If the property was acquired before the cutoff, the calculator uses holding period bands and the open plot slab table.

- Property type: Open plot

- Purchase cost: PKR 5,000,000

- Sale value: PKR 8,000,000

- Capital gain: PKR 3,000,000

- Holding period: ~2.5 years

- Slab band (open plot): >2 to ≤3 years

- Rate: 10%

- CGT: PKR 300,000

- Net proceeds after CGT: PKR 7,700,000

Why this happens: For older acquisitions, open plots step down gradually as the holding period increases.

Example 2: Same numbers, but bought on/after 1 July 2024 (ATL filer)

Now the acquisition date flips the regime, so holding-period slabs are not used in the same way. If the seller is ATL, the calculator applies a flat filer approach commonly summarized as 15% on gain.

- Property type: Open plot

- Purchase cost: PKR 5,000,000

- Sale value: PKR 8,000,000

- Capital gain: PKR 3,000,000

- ATL status: ATL (filer)

- Rate: 15%

- CGT: PKR 450,000

- Net proceeds after CGT: PKR 7,550,000

Why the tax is higher here: The calculator’s rate path is different because of the acquisition date.

Example 3: Flat bought before 1 July 2024 (rate can reach zero sooner)

Flats often reach a 0% slab earlier in the holding schedule compared with open plots.

- Property type: Flat

- Holding period: >2 years (pre-cutoff acquisition)

- Slab outcome: 0% in the slab table

- CGT payable (from slab): PKR 0 (for the CGT component)

How to use this example: It’s a quick check that your calculator is using the correct property-type slab when acquisition is pre-cutoff.

Example 4: Gain is zero or negative (sale ≤ cost)

If your sale value is not above your cost basis, your capital gain is zero or negative.

- Sale value: PKR 6,000,000

- Cost basis: PKR 6,500,000

- Capital gain: −PKR 500,000

- Expected calculator behavior: show “no taxable gain” and keep CGT at 0 (or not computed)

Why this matters: People often paste “sale value” into “cost” or forget a zero, producing a fake gain and an unnecessary tax estimate.

Common Mistakes People Make and Edge Cases

Most wrong answers from a capital gains tax calculator come from rate-selection mistakes, not math mistakes. Use these checks to avoid the common traps.

Mistake 1: Entering the wrong acquisition date

If you shift the acquisition date across the 30 June / 1 July 2024 cutoff, you can switch the entire regime.

Fix: Verify the date from your transfer/purchase documents before trusting any tax rate.

Mistake 2: Selecting the wrong property type

Open plot, constructed property, and flat can follow different slab rates for pre–1 July 2024 acquisitions.

Fix: Choose the property type that matches how the property is categorized in official paperwork.

Mistake 3: Confusing “sale value” with “capital gain”

Some people enter the gain as the sale value or forget to subtract the cost basis.

Fix: A pakistan capital gains tax calculator should compute gain for you. Enter:

- sale value (total consideration)

- cost basis (purchase cost)

Mistake 4: Ignoring holding period boundaries by a few days

For pre–1 July 2024 properties, crossing a threshold (like “≤2 years” to “>2 years”) can change the slab rate.

Fix: If you’re close to a boundary, test both disposal dates in the calculator to see the band change.

Mistake 5: Choosing ATL status based on assumption

For post–1 July 2024 acquisitions, ATL status is a major switch. Guessing here can produce a result that’s not useful for planning.

Fix: Confirm your ATL status close to the disposal date (since status can change with filing).

Edge case 1: Sale value equals cost basis

If sale value equals cost basis, the gain is zero.

Expected calculator behavior: CGT should be zero (or “not applicable”) and net proceeds should match the sale value.

Edge case 2: Negative gain (loss)

If sale value is lower than cost basis, capital gain is negative.

Expected calculator behavior: It should not show a positive CGT amount. Most estimators will show CGT as 0, but you should still keep records.

Edge case 3: Very small gains and rounding

Small gains can make the output look inconsistent if the calculator rounds the rate or tax too early.

Fix: Use a calculator that:

- rounds only at the final step, and

- displays both the rate and the tax amount clearly.

Edge case 4: Allowable expenses not included

Manual calculations may allow certain documented expenses to be added to cost basis. If your calculator uses a simplified “cost basis” field, it may not capture every situation.

Fix: Treat the tool as an estimate and keep a separate record of expenses to validate later.

How Our Capital Gain On Properties Tax Calculator Ensures Security?

This capital gains tax calculator is built to estimate tax without collecting personal identity details. You can use it for planning without entering sensitive information that could increase privacy risk.

What we do to protect your privacy

- No identity fields are required.

The calculator does not ask for your name, CNIC, address, bank details, or contact information. - Inputs are used only to compute the result.

The values you enter (dates, sale value, cost basis, property type, ATL selection) are only used to generate the estimate on the page. - No account is needed.

You can calculate without logging in or creating a profile, which reduces the amount of data exposure during use.

What “Share result” means (and how to use it safely)

The share feature is designed for convenience, but it can affect privacy depending on how it’s implemented:

- If the share link includes your inputs as URL parameters, anyone with the link can see those values.

- Treat share links like screenshots: share only with people you trust.

- If you are using a public device, use Clear All after you finish.

Practical safety checklist (before you share or save results)

- Double-check that no personally identifying notes are typed into numeric fields.

- Use “Copy all outputs” only when sharing with a trusted recipient.

- Clear the form on shared devices.

- If you suspect a scam or fake “tax help” message, avoid sharing screenshots or links that reveal transaction values.

How to Check Your CGT Estimate Before You Decide

Before you rely on any capital gains tax calculator output for timing or budgeting, do a quick validation. You’re not redoing the whole calculation—you’re confirming the calculator chose the right rule path.

If you want a quick sanity check on how much your price moved, use our Percentage change on price moves calculator.

1) Confirm the regime label matches your acquisition date

A reliable capital gains tax calculator for Pakistan should clearly show whether it is using:

- Pre–1 July 2024 (holding-period slabs), or

- On/after 1 July 2024 (ATL-driven treatment)

If the regime label doesn’t match your acquisition date, stop and fix the dates first.

2) Sanity-check the capital gain

Do a quick mental check:

- If your sale value is 8,000,000 and your cost is 5,000,000, your gain should be about 3,000,000.

- If your calculator shows a gain far from that, the inputs are likely swapped or missing zeros.

3) Verify the rate makes sense for your property type (pre-cutoff only)

If the property was bought before the cutoff, the rate should follow the slab table by:

- property type (open plot / constructed / flat)

- holding period band

If you selected “constructed property” by mistake, the slab can shift.

4) Check ATL status handling (post-cutoff only)

If the property is post–1 July 2024:

- Ensure the calculator used your ATL selection.

- If you are non-ATL, the calculator may require taxpayer type to choose an estimation path.

If you aren’t sure of your ATL status, treat the result as scenario planning: run both “ATL” and “Non-ATL” to understand range.

5) Compare the “tax payable” to the gain (quick proportion test)

As a quick check:

- A 10% rate means tax should be roughly one-tenth of the gain.

- A 15% rate means tax should be roughly 15% of the gain.

This simple proportional test catches most input errors instantly.

Limitations and Disclaimer

A capital gains tax calculator provides an estimate based on the inputs you provide and the rate rules it’s designed to apply. It is not a substitute for professional advice, official assessments, or document-based tax computation.

“Tools information on Calculatorgeek is provided for general guidance and educational purposes only.”

Key limitations to keep in mind

- Simplified cost basis: Some real-world expenses may be allowable in a manual computation if documented. A simplified calculator may not account for every expense category.

- Rule interpretation differences: Tax rules can be summarized differently across public guides. Always verify with official guidance when the decision is high-stakes.

- Status changes: Your ATL status can change over time depending on filing and compliance. A result based on “ATL” assumes that status is correct at the relevant time.

- Special cases: Certain property situations (e.g., specific legal structures, mixed-use cases, or unusual transfer terms) may require tailored treatment beyond a general online estimator.

Ad and Content Safety Note

This page is written to be safe for general audiences and advertising policies. It focuses on educational guidance, not promises or guarantees.

If you see ads on the page, they are shown by ad networks and are not recommendations. Always verify any tax-related claim using official documents or reputable professional advice before acting on it.

Author and Reviewer

Author

- Name: Daniel Harper

- Credential: CFP® (Certified Financial Planner)

- Role: Editor

- Bio: Daniel writes and reviews personal finance content with a focus on tax basics, real-estate decision support, and calculator-driven planning. He specializes in turning complex rules into practical checklists readers can verify.

Reviewer (Optional)

- Name: Ayesha Malik

- Credential: Chartered Accountant (CA)

- Role: Technical Reviewer

- Bio: Ayesha reviews tax and compliance content for clarity, assumptions, and calculation logic, with an emphasis on using official guidance and consistent definitions.

FAQs

1) What is a capital gains tax calculator pakistan used for?

A capital gains tax calculator pakistan estimates your likely CGT on a property sale by calculating the gain and applying the correct rate path based on acquisition date, property type, and filer status.

2) Does a capital gains tax calculator pakistan use my sale price or my profit?

It uses your profit (capital gain). Most calculators first compute sale value minus cost basis, then apply the applicable tax rate to that gain.

3) Why does my tax rate change when I change the acquisition date?

Because acquisition date can switch the entire regime. Many summaries treat 1 July 2024 as a key cutoff that changes whether holding-period slabs apply or an ATL-driven approach applies.

4) What if my sale value is lower than my purchase cost?

If your gain is zero or negative, many calculators will show 0 CGT. Keep documents anyway, because special cases can exist outside a simplified estimator.

5) How do I know the calculator selected the right slab?

Check the “Applicable regime” output first, then confirm property type and holding period (for pre-cutoff acquisitions). A good calculator shows the rate and why it was chosen.

6) Should I enter allowable expenses in the cost field?

If your calculator has only one “cost” field, you can treat it as a simplified cost basis. For filing decisions, keep a separate list of documented expenses and validate using official guidance.

7) Can I share my results safely?

Yes, but remember a share link may include your inputs. Share only with people you trust and use “Clear All” on shared devices.

REFERENCES (authoritative sources, 2–4 max)

- Federal Board of Revenue (FBR) — Budget 2024–25 Salient Features (Finance Act 2024 changes)

Confirms the key policy change: flat 15% CGT on gains for immovable property acquired on/after 1 July 2024 by ATL filers, regardless of holding period. - FBR — Income Tax Ordinance, 2001 (official consolidated text, amended up to 31 July 2025)

Primary legal text for capital gains framework (e.g., capital gains provisions and updated rules as consolidated by FBR). - PwC Tax Summaries — Pakistan (Individual): Income determination (immovable property CGT holding-period table)

Provides the commonly referenced holding-period slab table by property type (open plots, constructed property, flats) used for pre–1 July 2024 acquisitions. - EY Tax Alert — Pakistan Finance Bill/Act 2024 (technical summary of CGT change)

Technical summary confirming no change for properties acquired on/before 30 June 2024 and 15% for ATL filers for post–1 July 2024 acquisitions, with non-ATL taxed at applicable general rates.